How To Maximize Goodcover’s Renters Insurance

4 Jan 2024 • 7 min read

So, you’ve recently purchased a renters insurance policy. Congratulations!

At Goodcover, your protection is our top priority, and we want to ensure you get the most value out of your policy. Understanding the specifics of renters insurance and getting the most out of your policy can be tricky, but we’ll make everything transparent and guide you so that you can ensure your policy is tailored to your specific needs.

But that requires you to be part of the conversation. Together, we can tailor your insurance to fit your life, not vice versa.

This guide will provide you with the necessary information — from determining whether you need additional coverage for some items to understanding how deductibles and limits work — and provide actionable tips so you can maximize your renters insurance through Goodcover.

Let’s dive in.

1. Make a Home Inventory

2. Carefully Review Your Limits

3. Get Extra Coverage on Your Valuables

4. Adjust Your Coverage When Necessary

5. Keep Your Policy Details Updated

6. Change Your Deductible

7. Renew Your Policy on Time

8. Cancel Your Policy if You Need To

Throughout All of These, Don’t Forget To Contact Us

1. Make a Home Inventory

In case of property damage, your renters insurance policy covers your personal belongings. But you need to know how much your stuff is worth so you can get the best renters insurance policy.

We recommend doing a home inventory to ensure you get the coverage you need.

A home inventory will help you in two ways:

- Figuring out how much coverage you need is hard if you don’t know what you own and the values. A home inventory helps you create a list of everything in one place.

- Stress from a fire, theft, or natural disaster makes it hard to recall details from memory. A home inventory will help you quickly identify your losses and provide details to back up (also known as substantiate) your claims.

Listing every single thing in your home that renters insurance covers may sound difficult, but if you take it one step at a time, it’s easier than it sounds. Here’s a simple home inventory checklist to get you started:

- List valuables: Valuables aren’t just heirloom inheritances; they are anything of value that you own in your rental property. Furniture, appliances that you’ve purchased, clothes, and your laptop are all examples of valuables.

- Note their monetary value: Note the price of each item as you write it on your list. Receipt copies and photos of the item will help the claims process later.

- Know their location: Note where each item is located by room.

- Keep tangible records: If possible, keep receipts and records of these items, as it simplifies the claims process. If you don’t have receipts, check your credit card statements to see if the purchase is recorded there.

If you’re ready to get started now, our handy guide on how to create a home inventory includes a template that can get you started quickly.

2. Carefully Review Your Limits

Only you know how much coverage is enough. But chances are that your personal property is worth more than you think. Compare your personal property coverage limits to your home inventory.

Is your current coverage enough if something happens?

On the flip side, you also don’t want to pay for more coverage than you need for your stuff or personal liability coverage.

Our policy coverage limits start at $5,000 for personal property and $50,000 for liability coverage. Plus, with Goodcover, you can breathe easy knowing you can adjust your policy limits if your needs change.

Note: The prices for these plans vary per state. For a more accurate idea of the costs in your state, visit Goodcover's homepage and type your zip code in.

Once you determine how much coverage you need, you can change your plan and increase or decrease your limits if necessary.

3. Get Extra Coverage on Your Valuables

Some items just require a little extra, you know?

Whether for the fancy engagement ring you got last summer or the camera you plan on using to take honeymoon pictures, consider extended coverage for your high-value items.

You can upgrade Goodcover’s Standard plan to SUPERGOOD to get extended coverage for three item categories: jewelry, cameras, and musical instruments.

You’ll also enjoy extra perks and protections, such as zero deductible and coverage against accidental damage like water damage from dropping that camera into the surf at the beach.

Plus, Goodcover offers replacement cost coverage instead of using actual cash values (ACV), so you never have to worry about the depreciation value of an item. You’ll get the full amount needed, within policy limits, to replace the item.

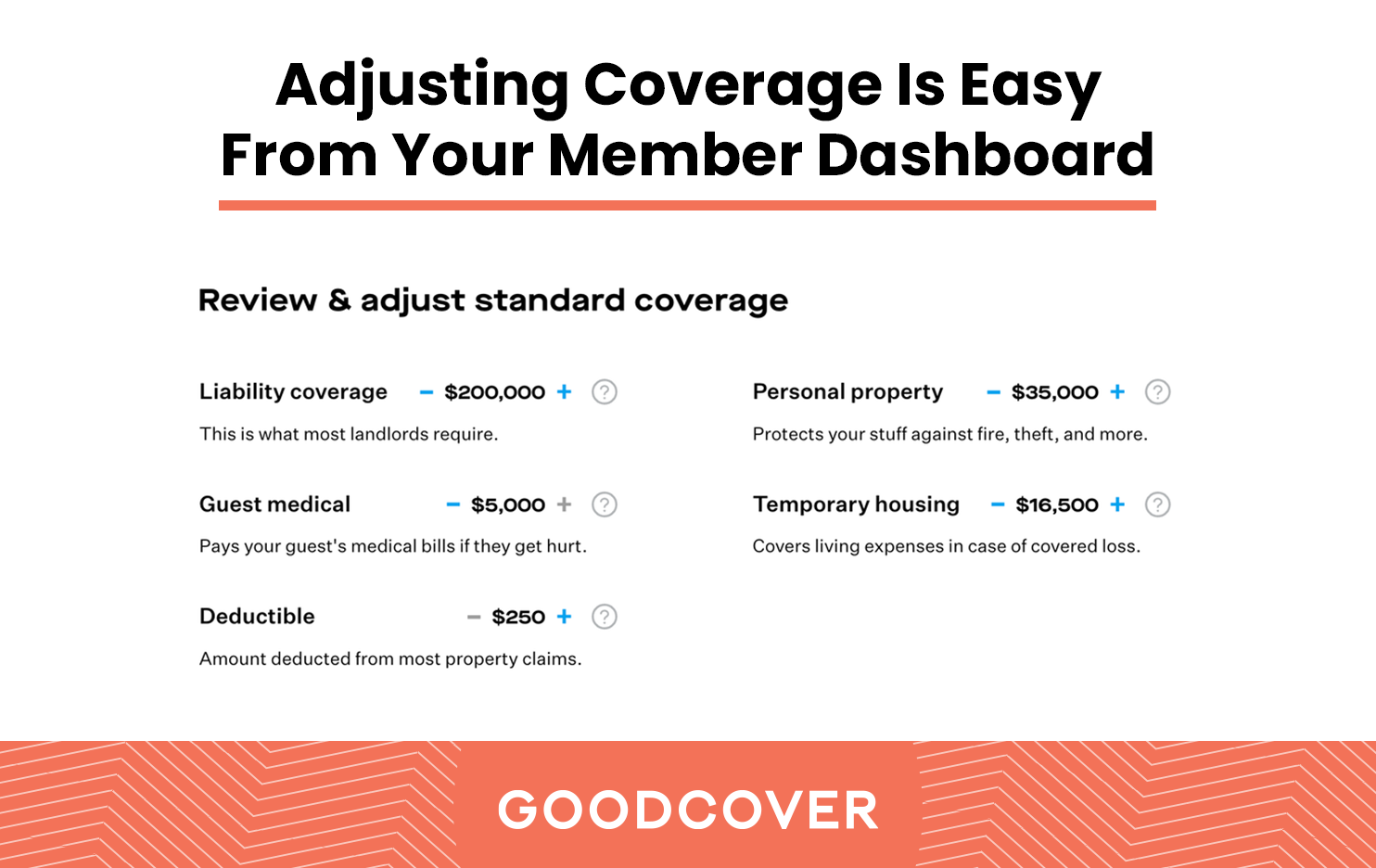

4. Adjust Your Coverage When Necessary

Change happens, and we allow you to upgrade or downgrade your policy anytime.

You can adjust your coverage and deductibles whenever you want, whether that's because you bought new stuff and need extended coverage or if you moved to a nicer area and aren’t as worried about certain perils (be careful with those cognitive biases, though).

Making changes is quick and easy – no lengthy procedures and no insurance agents. Just log in to your Member Dashboard, edit your coverage as required, and immediately see your new insurance premium.

5. Keep Your Policy Details Updated

Many renters get insurance simply because their landlord requires it – in fact, 75% of renters named that as their primary reason for having a policy. However, it’s important to understand your overall policy details – what your landlord requires (liability coverage) doesn’t cover your personal belongings – so you’ll need to select the coverage that’s right for you when you sign up, which is easy with Goodcover – your key to landlord-approved coverage. Additionally, your landlord will likely ask to be an additional interest in your policy.

Don’t worry; it doesn’t let them get your claim payments or anything like that. It just lets them check with your renters insurance provider to see if you have an active policy and if the amount of coverage meets the lease’s requirements

But be wary if your landlord asks you to add them as a named insured. Here’s a detailed blog explaining why you shouldn’t.

Your landlord will probably suggest adding your roommates, significant others, or family members as named insureds on your policy. Goodcover already protects everyone under your roof as long as they’re named on the lease, but you can add a second named insured from your Member Dashboard if necessary.

Only you (the policyholder) can make any changes to the policy.

If you or any person named in your renters policy moves to another property, you can always change the additional interests or second named insured through your Member Dashboard.

You’ll also need to keep your basic information up to date:

- Your address: If you move and still want coverage at the new location, you’ll need to provide the new address.

- Your payment information: Goodcover policies use autopay to give you seamless coverage. Always keep your credit card information updated to avoid any payment delays.

6. Change Your Deductible

Deductibles are fixed costs you pay out of pocket when you make a claim. As a Goodcover Member, you can adjust your policy deductible to ensure you get the most out of your renters insurance claims.

Our deductibles range from $250 to $1,000 to match different budgets, and you can even get zero deductible in some cases by upgrading to our SUPERGOOD coverage.

The latter is great for high-value items that would hike up the costs of your Standard policy.

7. Renew Your Policy on Time

Disasters don’t call you to warn you they’re coming, and the risk of having no renters insurance coverage when you need it isn’t worth it. We recommend renewing your policy as soon as the one-year term expires.

Review your policy limits, deductibles, and value of personal possessions when renewing, and adjust your policy to maximize renters insurance. If you’re unsure about how to make changes, contact us via email, phone, or live chat and we’ll guide you through.

8. Cancel Your Policy if You Need To

At Goodcover, your needs come first. So, if canceling your policy is what you need right now, we’re happy to help.

You can quickly cancel your policy by going to the Member Dashboard and clicking on the Cancel Policy button. You can also contact us to cancel the policy, check if you’re eligible for a refund, or have any doubts about the cancellation.

Throughout All of These, Don’t Forget To Contact Us

As your renters insurance company, we want you to get the most out of your Goodcover policy. So, if you need our support while following any of the renters insurance tips above, we’ve got you covered.

We offer 24/7 support for all Members. Whether you have questions about your policy or claims, you can contact us through these channels:

- For general queries and comments:

- Email: hello@goodcover.com

- Call: 1-855-231-GOOD

- To make claims:

- Email: support@goodcover.com

- Call: 1-855-231-GOOD

You can also contact us through the Live Chat option on our website or visit support.goodcover.com for claims.

Note: This post is meant for informational purposes; insurance regulation and coverage specifics vary by location and person. Check your policy for exact coverage information.

For additional questions, reach out to us – we’re happy to help.

More stories

Dan Di Spaltro • 10 Jul 2025 • 13 min read

Best Renters Insurance in Milwaukee: Your Guide to Coverage

Team Goodcover • 26 Jun 2024 • 8 min read

How to Get Renters Insurance

Team Goodcover • 17 May 2024 • 3 min read

Renters Insurance Facts: Debunking Common Myths

Team Goodcover • 12 Jan 2024 • 5 min read

Goodcover’s Complete Guide to Georgia Renters Insurance

Team Goodcover • 9 Jan 2024 • 6 min read