How Often Should You Shop for Renters Insurance?

20 May 2022 • 5 min read

If you're moving to a new apartment, renters insurance is probably one of the most important things you’ll need — and we’re not just saying that because we’re an insurance company.

Your landlord's insurance covers the building if anything happens but doesn’t protect your personal belongings if they get damaged or stolen while you live there. You may think you don’t have enough valuable items worth protecting or replacing, but if your entire apartment went up in flames, insurance money would help you rebuild your life.

Good news: unlike car or homeowner insurance, renters insurance premiums are pretty affordable. In fact, many people purchase it once, put their bills on autopay, and never shop around for a lower insurance premium. That's a mistake.

It's an excellent idea to re-shop your policy every year to ensure you're not missing out on better deals with a different company. Renters insurance is pretty easy to switch, so it’s worth your time to be sure you’re getting the best deal possible.

Today, we’re going over:

- How Often Should You Shop Around for Renters Insurance?

- How To Find the Best Renters Insurance That Suits You

- Final Thoughts: How Often Should You Shop Around for Renters Insurance?

How Often Should You Shop Around for Renters Insurance?

Goodcover recommends shopping for renters insurance annually, around renewal, to get the best possible deal. Insurance prices are regulated, but different companies charge more based on inflation or overhead.

Suppose the insurance provider you choose spends a lot of money on celebrity-endorsed commercial ads or has a lot of offices around the country. In that case, you'll likely see higher premiums since it costs more to run their business. Goodcover is ruthlessly efficient – we have eliminated all the waste and passed those savings on to you.

Another time to consider shopping around is when you have a significant life event, like getting engaged or moving to a new city.

How To Find the Best Renters Insurance That Suits You

The average renter may understand that renters insurance protects your personal property, but it covers much more. Understanding a little more about insurance is key to choosing the right policy for you.

You can break down getting the best renters insurance into the following process:

1. Understand What Renters Insurance Covers (and What It Doesn’t)

Here's what renters insurance covers:

- Personal property: This coverage protects your property, such as furniture, jewelry, musical instruments, art & collectibles, cameras, and electronics. It covers damage from perils such as fire, windstorm, explosion, water damage, theft, vandalism, and riots. The standard Goodcover policy comes with $10,000 worth of coverage for personal property, but you can bump that up depending on how much stuff you have.

- Personal liability protection: This coverage kicks in when someone sues you for bodily injury or property damage. It also pays for your legal defense if you need one. For example, if you cause a leak that damages your neighbor’s apartment below you, you can file a renters insurance claim for liability coverage. Goodcover policies start with $100,000 in personal liability protection, which most landlords require.

- Guest medical payments: This coverage pays your visitors' medical bills if they get hurt at your home, even if it's not your fault. This coverage comes in handy if someone falls in your house and sustains an injury.

- Temporary housing: Also called "Loss of Use" coverage, temporary housing can pay for additional living expenses if you can’t live in your house because of a problem covered by the insurance. For example, if your apartment catches on fire and you have to stay elsewhere while it’s being repaired.

Renters insurance doesn’t cover floods since the National Flood Insurance Program has a flood insurance policy. It also doesn’t cover your vehicles, powered boats, electric scooters, or aircraft.

While some electric-assist bikes are covered as bicycles on renters insurance, you should insure powered vehicles with auto insurance. But even then, Goodcover has your back. Members can access fair, competitive auto insurance rates through their Member Dashboard with Goodcover Auto.

For additional coverage, our SUPERGOOD package protects your jewelry, watches, musical instruments, and cameras from accidental damage, with no deductible. That's all in addition to your standard coverage, of course!

We also offer earthquake insurance in addition to your base Goodcover policy through our partner, Palomar.

2. Determine How Much Renters Insurance You Need

To determine how much renters insurance is right for you, you should create a home inventory. Create a list – with photos – of all your belongings and include dates of purchase, serial numbers, appraisal documents, and receipts to determine the value of your possessions and coverage limits. If you don’t have everything, just do your best to capture as much as possible.

Add all your expensive items, such as musical instruments, computers, smart devices, and jewelry, then figure out the cost of replacing them. Use that result to determine the minimum amount of renters insurance coverage you need.

Get enough renters insurance to help replace all your possessions if they’re stolen, lost, or damaged. Voilà, adulting!

3. Compare Different Insurance Companies Policies

Getting renters insurance quotes online or from insurance agents is pretty simple.

But when shopping around for renters insurance, make sure you’re basing your decision on price, coverage, and customer reviews to determine the best provider.

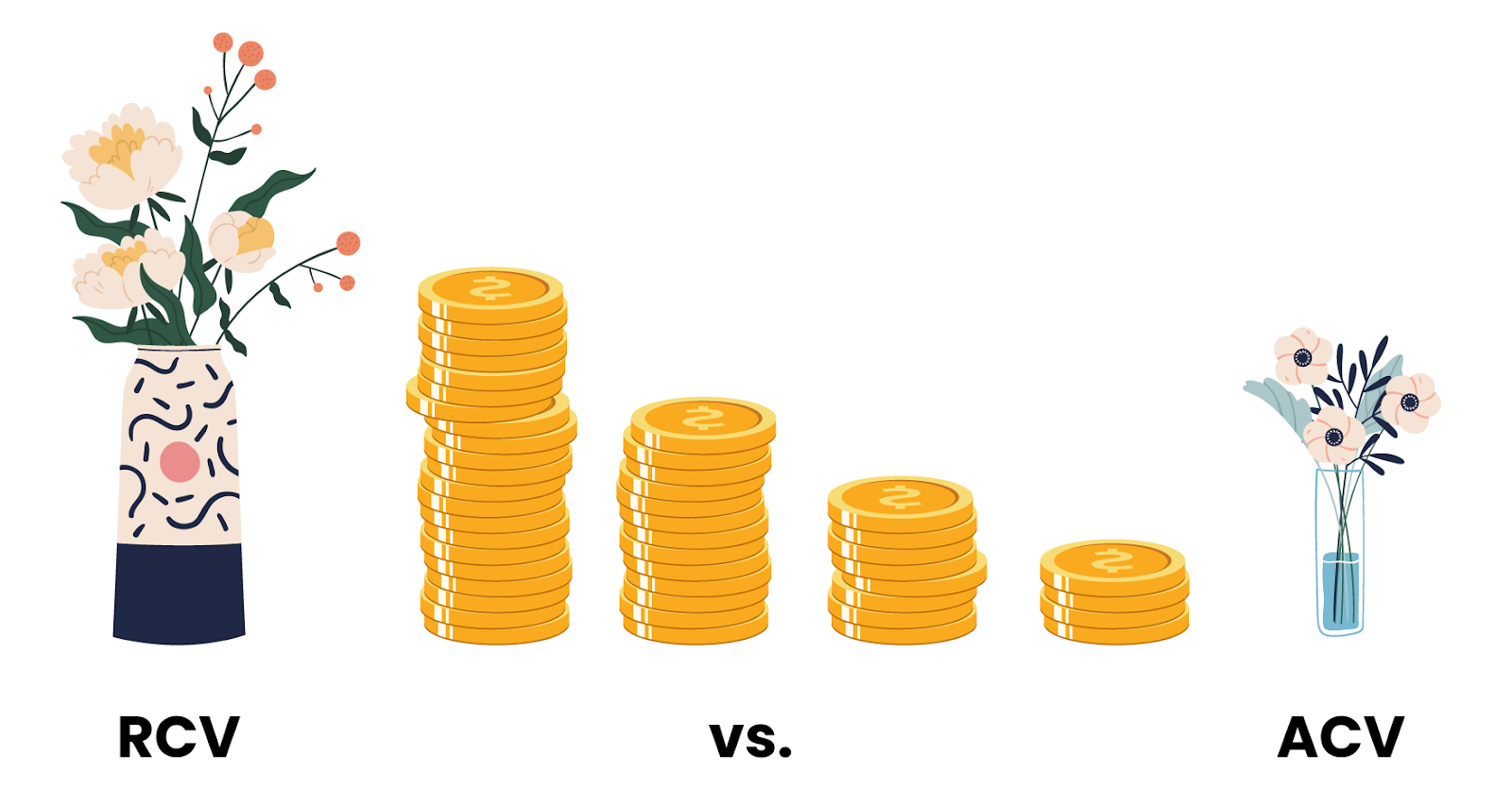

When shopping around for renter's insurance, one crucial factor to research is how you'll get reimbursed if you have a claim — actual cash value (ACV) or replacement cost value (RCV).

Actual cash value (ACV) is the reduced price of an item after considering depreciation — the price you get if you sell it in its actual status today. Replacement cost value (RCV) is the total retail price of a product without any depreciation, regardless of how much time has passed.

A good insurance plan provides replacement cost coverage while keeping your long-term benefits in mind. Goodcover offers RCV coverage as a standard for all renters' insurance policies (#humblebrag).

Goodcover can also compare different insurance policies for you. Email us at compare@goodcover.com for a fair review of your policy against what Goodcover can offer.

If you’re satisfied with your quote you can join immediately, and Goodcover will take care of canceling your old policy for you.

Final Thoughts: How Often Should You Shop Around for Renters Insurance?

When shopping for renters insurance, understand the renters policy you choose and get coverage at a reasonable cost.

At Goodcover, we are committed to pricing our services fairly and cutting out the extras like celebrity endorsements or agent fees. But Goodcover is not just about cutting waste. We make sure you're financially protected in the event of disaster or lawsuit.

Goodcover also returns any unused premiums to Members through its Annual Member Dividend. You can take that as a guarantee that we won't overcharge you and you’ll always know where your premiums are spent.

Switch to fair, modern, and cooperative insurance — get a Goodcover quote.

Note: This post is meant for informational purposes, insurance regulation and coverage specifics vary by location and person. Check your policy for exact coverage information.

For additional questions, reach out to us – we’re happy to help.

More stories

Dan Di Spaltro • 1 Jul 2025 • 14 min read

Renter's Insurance Boston: A Comprehensive Guide

Dan Di Spaltro • 27 Jun 2025 • 20 min read

Renters Insurance in Rhode Island: Costs & Coverage

Dan Di Spaltro • 26 Jun 2025 • 12 min read

Nashville Renters Insurance: A Complete Guide

Dan Di Spaltro • 25 Jun 2025 • 18 min read

Iowa Renters Insurance: Cost & Coverage Explained

Dan Di Spaltro • 24 Jun 2025 • 20 min read